Health & Fitness

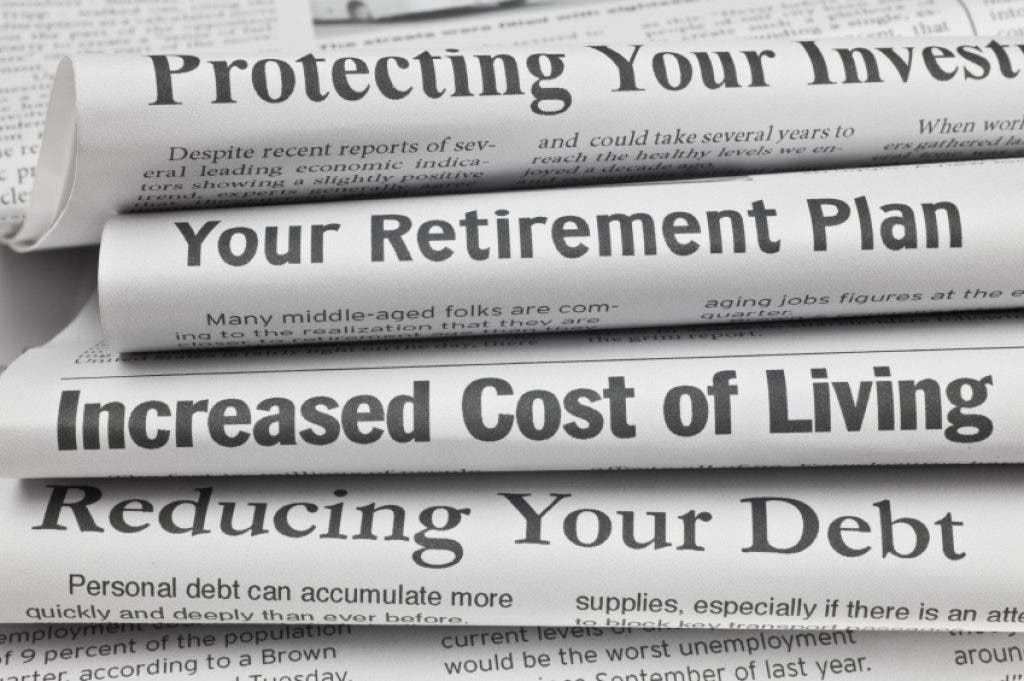

Inflation and Your Financial Plans

Inflation has been in the news a lot lately thanks to Federal Reserve policy. Here is a primer on inflation and what it means for your retirement plan.

There has been a lot of hand wringing in the media over the Federal Reserve's policy of "quantitative easing" and its possible inflationary repercussions. Regardless of Fed policy, prices of things we buy every day are heading higher, so I thought I'd make today's post a primer on inflation and what it means to our retirement plans.

What is Inflation and what causes it? The American Heritage Dictionary defines inflation as, "A persistent increase in the level of consumer prices or a persistent decline in the purchasing power of money, caused by an increase in available currency and credit beyond the proportion of available goods and services." Translation: Too much money chasing a limited supply of goods and services makes prices go up.

Inflation remains modest (says the government). The government measures inflation using the CPI, or Consumer Price Index. It looks at the price changes of a basket of commonly purchased goods and services over time. In its September news release, the government reported that prices for its entire basket of goods were up 1.7% from a year earlier. That doesn’t sound too bad. But over time even small amounts of inflation can have a big impact. A person retiring today who needs $75,000 per year in retirement income to cover his living expenses will need $105,000 per year to cover the same purchases after 20 years of inflation.

Find out what's happening in Bridgewaterwith free, real-time updates from Patch.

But what is YOUR inflation rate? Government statistics don’t tell the whole story. If you have been grocery shopping, filled up your gas tank, paid for medical care or health insurance, or paid your property taxes you might have a sense that your cost of living is increasing faster than the governments stated rate of inflation. And you might be right. Prices of different products go up at different rates. Everyone spends their money differently, and depending on what they purchase, each family has its own inflation rate. Heat your house with gas? Great, prices were down 11% last year. Heat with oil? Tough luck, your personal inflation rate will be much higher this year than your gas heat neighbor. If you spend a high percentage of your income on food, medical service, or property taxes (as is the case with many retirees) your inflation rate is probably has likely been running higher than the government figures.

So let us suppose your own personal rate of inflation in retirement will be 3%, which I think is a number which may be close to the actual cost of living change for many retiree. Now the $75,000 of living expenses in the example above will increase to $135,000 in 20 years. This is why your retirement plan needs to carefully consider the effects of inflation.

Find out what's happening in Bridgewaterwith free, real-time updates from Patch.

Will inflation get worse? Why worry? Well consider that if inflation rises to 7%, your cost of living will DOUBLE every 10 years, and QUADRUPLE every 20 years. That $75,000 per year you need to retire at 65 would increase to $300,000 per year at 85! Many retirement plans simply would not be able to keep pace! Such an outcome (or worse!) is indeed possible over the long run. The good news is that I believe that very high inflation is unlikely over the next few years. You are likely to see a dramatic increase in some grocery prices, meats in particular, due to this year’s Midwest drought. But lasting inflation is another story. As the definition above states, inflation is caused by too much money chasing too few goods and services. And central bankers from Europe to Japan and our own Federal Reserve are certainly printing a lot of money. It is the second half of the definition that may put the lie to the notion that the United States is heading down the same road as Zimbabwe or Weimar Germany. We are not suffering from any shortage of goods and services. In fact, the economy has an overabundance of supply. Oversupply of labor (aka high unemployment) and excess factory capacity should keep enough downward pressure on prices to prevent hyperinflation from taking hold anytime soon. However, if the economy were to suddenly accelerate however, we could see a very significant increase in inflationary pressure.

So what should an investor do? The only real protection against the ravages of inflation is to keep your money growing faster than inflation eats it away. We financial types think in terms of a “real” rate of return, which is the rate of return you earn on your money AFTER inflation takes its cut. Let’s say you own a bank CD paying 1.25%. This is its “nominal” yield. After 3 years of compounding, the bank pays you $10,379 on your original $10,000 investment. But during those same 3 years, the value of that money, its “purchasing power” has fallen. The “real” rate of return is the difference between what you earn (1.25%) and your personal inflation rate (lets say 3%). Your real rate of return is negative 1.75%. The $10,379 you will get 3 years from now will only be able to buy $9,484 worth of stuff. If inflation is 3%, any rate of return less than 3% means your money is shrinking in value, any return greater than 3% means your money is growing.

Inflation busting investments? During inflationary times, fixed income investments tend to fare poorly. Interest rates will rise, and many fixed income investments will lose money. Cash by definition will lose value. Unfortunately many retirees are heavily invested in these more conservative investments, which may magnify their misery if inflation increases. Stocks may retain value, since companies can raise prices in response, and profits may increase. But rising interest rates and other costs may weigh on profits as well, so stock investments are not a perfect inflation hedge. “Real” assets, owning “things” may do better when prices rise. Gold and other precious metals are a classic inflation hedge. So are commodities (metals, energy, agricultural products, etc.) and commodity producers, and real estate (although the latter may suffer if interest rates soar). Adjustable rate fixed income investments and TIPS (Treasury inflation protected securities) may offer some protection in the fixed income sector.

Diversify, Diversify! I do not recommend committing an entire investment portfolio to any particular macroeconomic outcome. Despite what you hear from talking heads on TV, inflation is NOT an automatic and inevitable result of the governments easy money policy. Real life is much more complicated than that. However, it is wise to consider the potential impacts of possible inflation on your retirement plan and devote a portion of your diversified portfolio to investments which offer some protection from rising prices. A well diversified portfolio with broad exposure to many different asset classes (including those mentioned above) should be able to fight inflation without relying on it!

Help is Available. It is a complicated world out there! If you need help designing a diversified portfolio for your retirement or other assets, or if you haven’t yet taken the time to create a formal financial plan, get some professional help. A Certified Financial Planner(tm) is ethically required to put your financial needs ahead of his own, and can help you weigh and balance various financial risks. You can learn more about the process of creating a financial plan at www.letsmakeaplan.org.

Important Note: Investing entails risk. Investment strategies cannot guarantee against losses, including losses in purchasing power. Consult with your investment advisor before acting on strategies mentioned in this artlcle.